Getting the balance right between your cash holding, emergency fund and investments

Aaron Pitt, Chartered Financial Planner at Kellands Bristol, takes a look at this perennial issue.

The idea of keeping a rainy-day fund to cover any unforeseen events or saving towards short term goals is the first part of any financial plan. The money is secure, often protected by the Financial Services Compensation Scheme (FSCS) and ostensibly will not fall in value. Your deposits form a firm ground from where your investments can stand and grow over the medium to long term.

What is inflation

However, just because your deposit accounts are slightly increasing each year, it does not mean you are making money. The opposite is often true. When considering inflation, especially in the current low-interest climate, your cash deposits are losing money in real terms.

Have ever felt that your weekly shop is getting more expensive, or that a chocolate bar is smaller than it used to be? If so, you are feeling the effects of inflation. Inflation is the general increase in the price of products over time. The Office for National Statistics (ONS) measures inflation on an ongoing basis and publishes the figure monthly. This is known as the consumer price index (CPI). According to ONS figures, inflation has been as high as 8.4% and has even been below 0% for a while in 2015. Whilst the UK Government set a target of 2% per year, following the events of 2020, we may well see it go higher in the future.

Effect of inflation on your savings

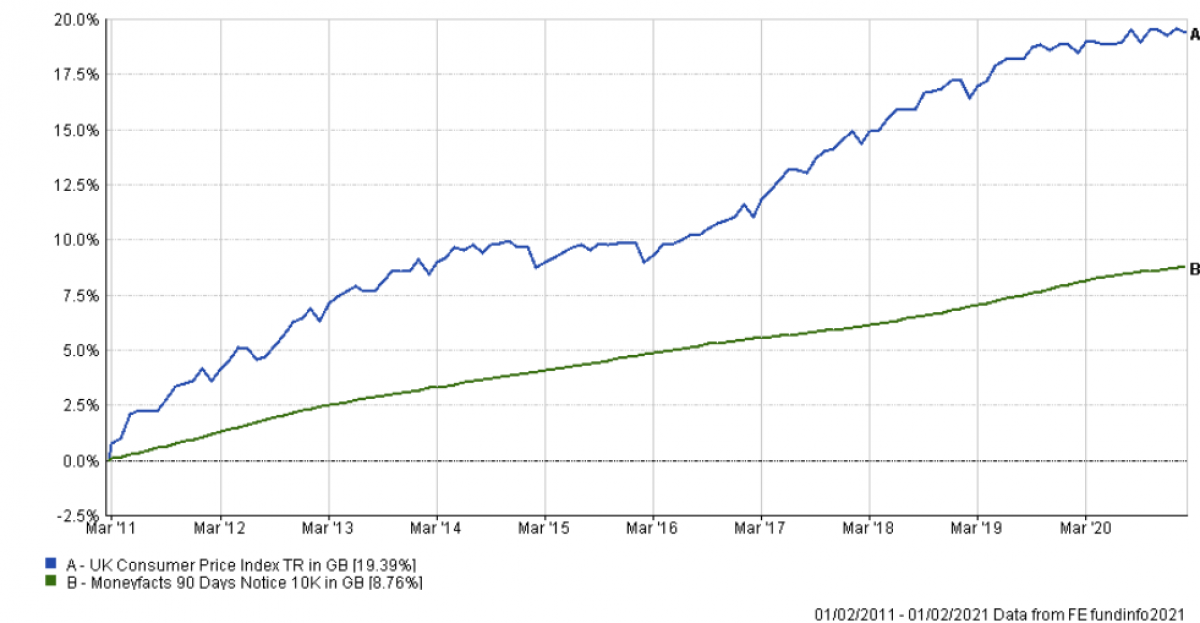

If your deposit accounts are producing returns lower than inflation, you are losing money in real terms. With interest rates nearly at an all-time low, cash savings will rarely outperform inflation. The graph below shows a comparison of inflation, measured by CPI, and deposit account interest over ten years. As you can see, total inflation was nearly 20%, and a deposit account returns 9% - a difference of 11% or 1.1% per year on average. The effect this has on your cash holding is significant, especially if you do not actually need the cash on deposit. For example, holding cash of £100,000 equates to a loss of £1,100 per year or over £11,000 in ten years.

The figure is even more concerning when compared to the average performance of an investment portfolio. Since 2011, the mixed investment cautious, balanced, and growth sectors have performed 45.41%, 60% and 84.57%, respectively1. Compared to the 8% of a deposit account, this is a difference of up to 76.57% or 7.66% per year. This is illustrated in the graph below. Basing this on £100,000 again, it is equal to £76,570 over ten years.

Alternative investment strategy to cash

The worry for many potential investors is that the stock market is volatile, and investments can, and do, go down over the short term. With many of our clients, we seek to combat this in two ways. The first has already mentioned - ensuring that you have enough cash on deposit so that if the markets go down, you have a sensible emergency fund. The second is using a split investment pot strategy.

A split pot strategy means having two parts to your portfolio; a low-risk part and a higher risk part. The idea is that the lower risk part will have lower volatility. It is likely not to perform as well as the higher risk part but hopefully it will return more than inflation and cash. If you did need money from the portfolio, it could come from the lower risk part, leaving the higher risk part to grow over the long term. We see this as a step between total risk investment and cash, reaching a good balance of risk and return.

How much cash is too much cash?

In terms of how much cash should you actually hold, there is no ‘one size fits all’ cash balance - we are all different after all. There are, however, a few questions that you can ask yourself to work out a sensible amount.

- The first calculation is to see how much you spend per month, multiply this by six, and you have a sensible emergency fund. Following this, it is a little more arbitrary

- Do you have any upcoming significant purchases in the next three to five years, for example: new car, holidays, home improvements, high-cost debt

- Work out your short-term financial objectives

With an idea of your emergency fund, your short-term needs, and your short-term objectives, you will begin to have a good idea of the amount of cash you need on deposit.

Objective planning is complicated, and asking yourself the correct questions to get to where you would like to be can be even more difficult. Creating a structured long-term plan with a Financial Planner is a great way to begin your journey. Contact Kellands today, to find out how we can help.

Article written by Aaron Pitt, Chartered Financial Planner at Kellands Bristol.

Important information

Any views or opinions expressed are provided in good faith and should not be relied upon in isolation to make informed investment decisions but instead should be considered in conjunction with other relevant information which is available, including that which is held within the public domain.

The information provided within this summary is based upon our understanding and experiences of investment markets, which is subject to change without notice.

Please note that past investment performance is not a guide to future performance. The potential for profit is accompanied by the possibility of loss. Values of investment funds may go down as well as up. Any figures provided are for illustrative purposes only and are not guaranteed.

1Figures produced using FE Analytics; portfolios are based on the Investment association 0-35%, 20-60% and 40-85% sectors.